- No products in the cart.

Forecasts predict a bumpy ride for residential building but a more favourable medium- term outlook for non-residential and civil construction

September 28, 2022

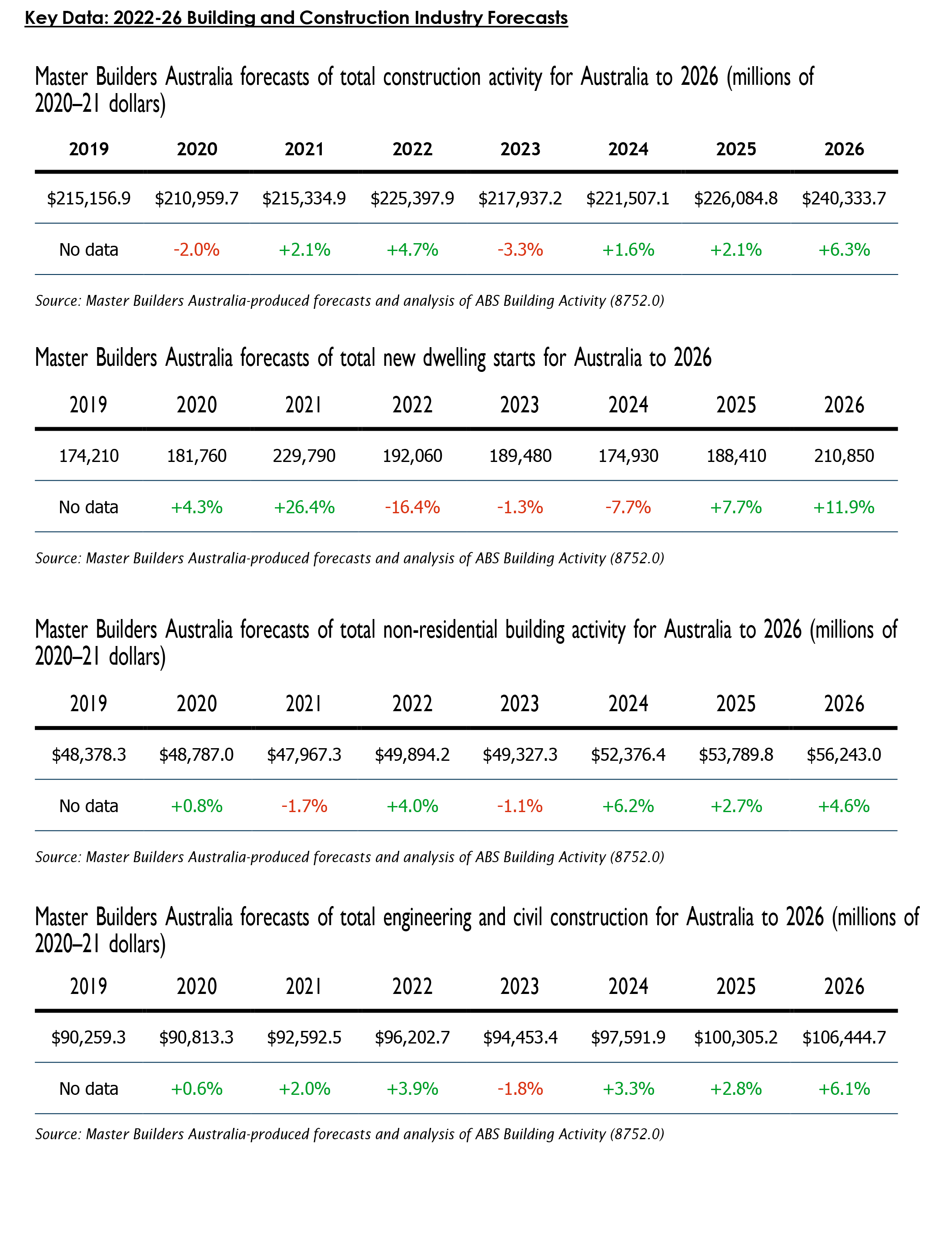

Master Builders Australia has today released an update to its forecasts for the building and construction industry out to 2026.

In the post-pandemic economic environment of interest rate rises, surging inflation, and unemployment at a 50-year low, the latest forecasts indicate that activity is still likely to expand modestly over the medium term despite the effect of short-term challenges. However, there will be considerable variation in the pattern of growth by subsector.

Even though about 200,000 new homes need to be built each year to accommodate long-term population growth, we are likely to fall significantly short of this until 2026. Activity on the medium-high density side of the market is likely to be particularly slow.

“While pandemic conditions brought forward some residential building demand, the current economic conditions of interest rates hikes, inflation increases, and continued shortage of workers and materials, are significantly contributing to the decline”, according to Master Builders Australia Chief Executive, Denita Wawn.

Long-term supply constraints continue to hamper residential building, with Master Builders Australia supporting the decision by the Federal Government to establish the Housing Supply Council in conjunction with State and Territory Governments.

“Our members continue to be frustrated with lengthy delays in approvals for land title, building applications, and occupation certificates. Shortage of land in the right places, high developer charges, and inflexible planning laws also restrict opportunities to meet the housing needs of our future. These long-term supply challenges are the responsibility of State and Territory Governments”, said Mrs Wawn.

The outlook for non-residential building activity (social, cultural, retail, commercial and warehousing) is reasonable with a small decline in 2023 but steady increase from 2024 to 2026.

“Master Builders remains concerned about the potential impact of unfavourable changes to the industrial relations framework for non-residential activity. Changes already made and intended are likely to mean higher costs and lengthier rollout times. Were it not for these changes, the forecast growth rates would be more substantial”, said Mrs Wawn.

Civil and engineering construction is likely to show the strongest performance of the three sectors of the industry and while a small decline is forecast for 2023, growth is forecast for 2024-26. However, the industrial relations changes currently under implementation will prevent growth here from reaching its full potential over our forecast horizon and beyond.